Leveraging Relationships

SAIB strives to develop long-term relationships and collaborations through partnerships. Communications and relations with stakeholders, particularly customers, business partners, and investors, need to be seamless and effective while complying with regulatory requirements and Bank policies.

Investors are stakeholders who provide the Bank with the capital it requires to operate; the Bank thus has a responsibility to be transparent with its investors about all aspects of its performance, its policies, forecasts for future performance, future plans, strategies, and risks. SAIB also complies with regulatory requirements and its own policies by disclosing information to the general public through the media, its website, and on the Tadawul.

The Articles of Association and corporate governance rules of the Bank express the rights of shareholders, the guidelines for relationships with them, and the mechanisms for exercising their rights. These are also governed by the Saudi Company Law. The rules and procedures for shareholders to exercise their rights, including rights relating to dividends, convening meetings, attendance and participation at meetings, voting rights, and rights to information. A provision for shareholders to make complains also assures that they will be attended to and are entitled to a reply detailing any action taken in response to their complaint.

As of December 31, 2019, the market value of the Bank’s ordinary share was SAR 18.04 as against SAR 17.12 on December 31, 2018. During the year, the highest share price recorded was SAR 21.44 on January 28 and the lowest share price recorded was SAR 14.98 on November 3.

The breakup of the shareholdings as at December 31, 2019 is as follows:

| SAR million | 2019 | 2018 | ||

| Amount | % | Amount | % | |

| Saudi shareholders | 6,750.0 | 90.0 | 6,750.0 | 90.0 |

| Foreign shareholders | – | – | – | – |

| Mizuho Corporate Bank Limited | – | – | 187.5 | 2.5 |

| Treasury shares | 750.0 | 10.0 | 562.5 | 7.5 |

| 7,500.0 | 100.0 | 7,500 | 100.0 | |

| For the years ended December 31 | 2019 | 2018 | 2017 |

| Value, SAR million | 13,530 | 12,840 | 11,325 |

| Percentage of total market capitalisation | 1.96 | 2.07 | 2.42 |

| Key performance indicator | 2019 | 2018 Restated |

2017 | 2016 | 2015 |

| Share capital (SAR million) | 7,500 | 7,500 | 7,500 | 7,000 | 6,500 |

| Total shareholders’ equity (SAR million) |

12,007 | 11,621 | 13,494 | 12,833 | 12,036 |

| Basic and diluted earnings/share (SAR) | 0.17 | 0.65 | 1.83 | 1.40 | 1.90 |

Personal Banking

SAIB aims to deliver a superior personal banking service by being closer to the customer and understanding them better, thus building a relationship with them and being their long-term financial partner. The Bank tailors its offers with the customer’s situation and requirements in mind and makes banking simpler and more accessible to them; this overall approach to the customer ensures their financial prosperity in the short and long-term. By understanding the needs and preferences of the customer, the Bank assists them in financial planning to protect their wealth and ensure that expected future cash flow requirements can be met, facilitating their financial and asset growth.

During the year, the Bank concentrated on improving its digital capabilities and automation, launched new digital sales channels to widen the Bank’s reach and footprint, and looked to the Financial Technology (Fintech) space to disrupt its own business model and envision new and sustainable opportunities for growth.

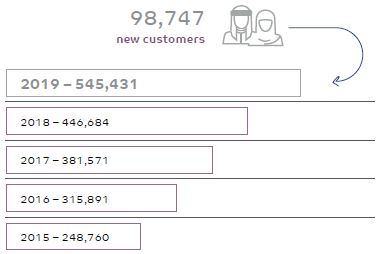

The Bank continued to grow the personal banking customer base, acquiring 98,747 new customers during the year under review.

The Bank conducts customer satisfaction surveys, which indicate a high degree of satisfaction.

The Bank has achieved almost uniform results in overall customer satisfaction across regions.

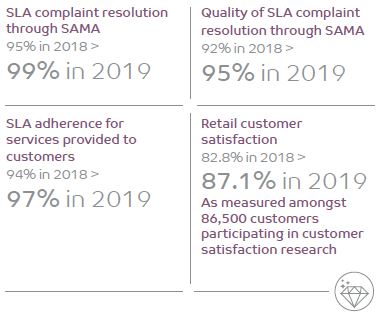

The Bank works diligently to resolve complaints effectively and efficiently to boost customer satisfaction, resulting in a strong performance of 95.43% of complaints being resolved within five days.

| Criterion | Unit | Year | ||||

| 2019 | 2018 | 2017 | 2016 | 2015 | ||

| Complaints registered | Nos. | 30,332 | 26,497 | 14,523 | 9,897 | 7,907 |

| Complaints resolved within five days | % | 95.43 | 96.53 | 99.03 | 98.06 | 99.00 |

GRI 103-1, 103-2, 103-3, 418-1

SAIB continued its digitalization and automation efforts that are centred around maximizing convenience to the customer. Internet and mobile banking, self-service kiosks, ATMs, Cash Deposit Machines (CDMs), and Interactive Teller Machines (ITMs) are reducing the reliance of customers on manual transactions and branch visits during opening hours to conduct their transactions with the Bank. Approximately 98% automation has been achieved in processes such as new account opening and new card issuance. The Bank intends to widen its reach by setting up more self-service kiosks across the Kingdom, rather than increasing the number of branches. Customers are continuously encouraged to migrate from manual processes to online processes and this has been a successful endeavour, with the incidence of online processing during the year under review growing to 94% from 92% in 2018.

| Access point | Year | ||

| 2019 | 2018 | 2017 | |

| Branches | 52 | 52 | 49 |

| Ladies sections | 10 | 11 | 12 |

| ATMs (multi-function) | 52 | 51 | 49 |

| ATMs (dispense) | 341 | 361 | 372 |

| CDMs | 12 | 12 | 10 |

| Interactive Teller Machines | 4 | 4 | 4 |

| POS terminals | 9,375 | 9,307 | 9,178 |

The means through which the Bank communicates with its customers has also shifted towards electronic channels.

| Initiative type | Year | ||

| 2019 | 2018 | 2017 | |

| Marketing campaigns | 165 | 153 | 45 |

| Events | 45 | 62 | 85 |

| Emails to customers | 12,853,809 | 10,612,267 | 95,000 |

| Press releases | 44 | 54 | 54 |

| Unique visitors per month to SAIB website | 222,552 | 215,906 | 179,432 |

| Page views per month | 1,318,118 | 1,002,738 | 732,875 |

| Twitter followers | 974,786 | 928,000 | 845,347 |

| Facebook fans | 1,281,011 | 1,298,437 | 1,317,206 |

| Instagram followers | 47,973 | 36,200 | 27,497 |

| Snapchat views | 1,000 | – | – |

The e-channels have proven to be popular, as indicated by penetration statistics and customer surveys indicating a high degree of satisfaction.

The Bank has adopted changes to the decision-making process to facilitate responsible banking. A 360-degree survey of the customer’s situation that includes an evaluation of their disposable income based on their family situation and expenses is used to make financing decisions. This helps to lower the repayment burden on lower income customers while enabling the Bank to be more flexible with the amounts loaned to higher income clients.

The Bank recognizes the increasing presence of women and millennial customers in the market and as key members of society in accordance with the Kingdom’s Financial Sector Development Program (FSDP), and seeks to broaden its product portfolio to cater to these burgeoning segments. To this effect, the Bank has introduced sales for most of its products through telesales, enabling easier and more convenient access for these segments. Further improving convenience for these segments, most of the Bank’s branch services have been moved to Flexx Touch. Furthermore, the Bank’s Fintech vision and technology initiatives are crafted with consideration given to the preferences and accessibility of millennial customers. Going forward, the Bank aims to be a key player in the digital space and is constantly enhancing its internal capabilities to achieve its ambitions in this space.

Corporate Banking

SAIB’s corporate banking function serves a wide range of clients such as large corporates, mid-sized corporates, and the MSME sector. The Corporate Banking Business Group of the Bank operates rom three regional headquarters based in Riyadh, Jeddah, and Al-Khobar. The Bank’s wide range of technology-enabled products help to meet the needs of clients, including Islamic banking products. The Bank also leverages its subsidiary and associate companies to provide the following products and services:

- Alistithmar Capital: Investment services

- American Express (Saudi Arabia): Corporate cards

- Amlak International: Real estate financing

- Saudi Orix: Leasing

- Medgulf: Insurance

For the year under review, the Corporate Banking Business Group maintained a resilient performance during what were challenging economic conditions. The Group focused on SAIB’s key competitive advantage, which is its close relationship to its customers and agility to address their financial needs. Emphasis was placed on growing the commercial banking segment and MSME customer base, while reducing credit concentration. The Group continues to support initiatives aligned with Vision 2030.

Growth in customer base

| Customer type | Year | ||||

| 2019 | 2018 | 2017 | 2016 | 2015 | |

| Corporate banking | 1,650 | 1,540 | 1.450 | 1,407 | 1,367 |

| MSME | 11,109 | 11,940* | 15,936 | 13,704 | 10,441 |

*The reduction in MSME accounts during 2018-2019 was due a clean up of abandoned accounts.

The customer experience is one of SAIB’s key strategic priorities. This key to enhancing the customer experience for the Bank is utilising its competitive advantage – customer insight. The Bank conducted extensive internal testing of its quality assurance services, as well as conducting customer surveys and analytics to better understand its customers and how to enhance their service experience. To achieve this, an in-house specialised quality assurance and analytics team highly experienced in cognitive analysis and computer system experience helped the Bank to add value to how customers interact with and experience the Bank’s services. Initiatives undertaken during the year primarily focused on enhancing the customer experience around online account opening and printing cards through kiosks, and launching new finance and refinance products through the digital Flexx Touch platform.

Operational excellence

The Operational Excellence Team’s objective is to enhance the experience of SAIB customers. The team optimises processes through Agile and Six Sigma practices and utilises various data research and reporting methodologies to measure and manage the performance of the business.

During the year under review, the team continued to elevate the performance and quality of service provided to SAIB’s customers. A dedicated SLA monitoring unit was established to actively monitor all customer requests and ensure adherence to SLAs, thus contributing to the increased SLA adherence observed in 2019. The unit also highlights possible improvements to the Operation Excellence SIGMA teams for process enhancement. The SLA measurement method was also enhanced in CRM to measure the SLA performance on a department level, enabling the SLA monitoring unit to identify individual departments and steps in service delivery that may have an impact on service delivery performance. Over 23 Corporate Banking Services were onboarded to CRM to implement and measure SLAs.

During the year, 10 process improvement projects were completed, aimed at optimising and standardising process flows. Key projects completed include talent acquisition, outsourcing of staff salary payments, corporate cash deposit card issuance, POA enrolment and validation, and online complaint handling. Moreover, governance of Product Approval Memorandum (PAM) and Service Approval Memorandum (SAM) is now centralised. A transformation project was also conducted in the Tele Sales Department that saw the organization structure being restructured for efficiency, systems being enhanced, and the sales processes being re-engineered. Additionally, a training and manpower plan was developed to meet the expected output in 2020.

Customer satisfaction was recorded in relation to the overall customer experience with SAIB’s digital channel, RIB and CIB. An increase in satisfaction from 82.8% in 2018 to 87.1% in 2019 was registered as a result of enhancements made to the RIB menu based on a customer experience study conducted in coordination with the e-channel team. Efforts to improve customer satisfaction continue with the launch of a new SMS survey module that will enable the effective measurement of customer experience and feedback. The survey module allows for a custom survey based on service, product, and customer segments and other factors related to better support decision making by business lines.

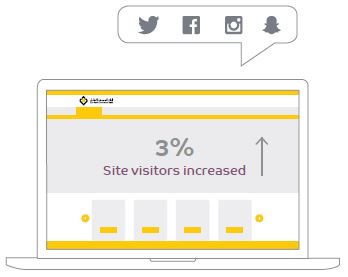

SAIB made extensive use of the electronic medium to connect with and engage its customers. The Bank’s corporate website was redesigned in 2018 to make it more user friendly and has seen increased activity since. Site visitors increased by 3% from 215,906 to 222,552 during the year, with page views increasing 31% from 1,002,738 to 1,318,118.

SAIB continued to have the most prominent social media presence among Saudi financial institutions. The Bank also continued to grow its base of followers on all social media platforms such as Twitter and Instagram.

The Bank also continued to increase the use of emails to communicate with its customers. 12,853,809 emails were sent to customers, an increase of 21% over 2018.

The Bank's loyalty programmes, Aseel and WooW, continue to grow year on year.

Aseel partners have grown to 506 partners in 2019, compared to 493 in 2018.

WooW has seen record enrolment and redemption metrics in 2019. Innovation and digitalization remain at the forefront of the programme. The customer experience will continue to be enhanced with redemption being made much easier in 2020.

- The Travel Card Campaign, ‘حطها على يمناك’, was launched in mid-2019 to drive Travel Card usage, grow customer acquisition, increase card issuance, and further promote the SAIB brand. This Above the Line (ATL) campaign targeted existing and non-customers, with Riyadh and Jeddah Airports being branded with campaign messages alongside strategic locations within the cities through the use of billboards. The year also marked the official launch of 100 currencies with the Travel Cards.

- The Apple Pay campaign was launched to promote the increased usage of SAIB cards.

- WooW Summer, a Below the Line (BTL) campaign, was launched to increase customer engagement and raise awareness of the programme.

- Cards Summer, a BTL campaign, was launched to increase card usage and transactions locally and internationally.

- The Saudi National Day BTL campaign aimed to increase engagement through SAIB’s social media channels.

GRI 102-9, 102-10, 103-1, 103-2, 103-3, 204-1, 308-1, 414-1

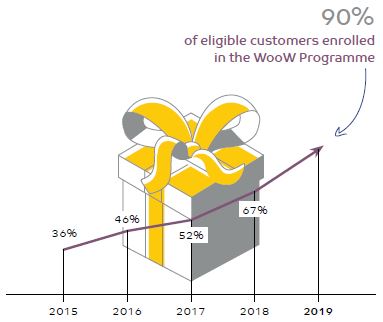

Through the WooW loyalty programme, SAIB rewards its loyalty members with points for their transactions. Members can then redeem these points for various gifts through the WooW e-catalogue. The WooW programme continues to achieve the programme's strategic metrics, with 90% of eligible customers enrolled.

WooW Surprise campaign

The WooW Surprise campaign was launched on social media during the holy month of Ramadan to raise brand awareness and engagement.

WooW Summer campaign

The WooW Summer digital campaign targeted SAIB customers to create awareness and engagement about the SAIB WooW programme.

SAIB maintains strong relationships with its business partners, ensuring the uninterrupted conduct of its operations. The Bank has established long-term relationships with its vendors and service providers that are based on mutual trust and confidence, and is ethical and transparent in its dealings with them. The Bank’s procurement costs are primarily focused on utilities, stationery, equipment, and software. SAIB is conscious of its impact on the local economy and local communities and sources from Saudi suppliers whenever possible. The performance of suppliers undergoes regular reviews to ensure the timely procurement and quality of supplies as well as maintaining good relations; the Bank also ensures the timeliness of its payment obligations.

SAIB’s network of correspondent banks serves the MENA, European, African, and North American regions and is crucial in supporting the Bank’s overseas transactions.

Visa Inc. recognized the SAIB Travel Card, which saw the introduction of 100 currencies – the largest selection of currencies available in a travel card in the Central Europe, Middle East, and Africa region, as the ninth largest programme of its type across the globe.

For the year under review, the Bank prepared detailed performance reports on each of its business partners, highlighting the background, products, market analysis, financial analysis, major risks and mitigation, valuations and recommendations, and presented to ALCO and the Board.

Alistithmar Capital launched a new income generating real estate fund.

| Year | |||||

| 2019 | 2018 | 2017 | 2016 | 2015 | |

| International suppliers | 137 | 39 | 79 | 24 | 25 |

| Local suppliers | 305 | 148 | 154 | 80 | 65 |

| Spending (international procurement) – SAR | 68,244,427 | 60,777,564 | 36,644,044 | 25,000,000 | 7,000,000 |

| Spending (local procurement) – SAR | 399,433,627 | 389,513,667 | 259,314,171 | 130,000,000 | 83,000,000 |

GRI Community member

SAIB retained its GRI Community membership for the year under review. The GRI Community is an inclusive and collaborative network of companies and stakeholders committed to transparency and quality sustainability reporting.

UN Global Compact status

The UN Global Compact is an initiative which companies voluntarily participate in to align their strategies and operations with universal principles on the environment, labour, human rights, and anti-corruption.

SAIB retained its UN Global Compact (GC) status for the fourth year based on its Communication on Progress (COP) submission, demonstrating its commitment to and leadership in corporate sustainability governance. The submission met the minimum requirements and qualified for the GC Active level, and is publicly available on the Global Compact website.

International Integrated Reporting Council (IIRC)

SAIB was the first entity in the Middle East to join the International Integrated Reporting Council Business Network. Through this membership, the Bank benefits from the experience of over 1,750 international participants and has peer-to-peer contact with reporting practitioners. Furthermore, the membership is an affirmation of the Bank’s desire to make a significant difference locally and internationally by supporting better investment decisions and contributing to improve capital allocation and longer-term growth.

SAIB maintains healthy relations with its regulators. In December 2018, the Bank reached a settlement with the General Authority for Zakat and Tax (GAZT). The Bank’s Zakat assessments for the period between 2006 to 2018 amounted to SAR 775.5 million, to be paid on the agreed upon schedule:

| SAR ’000 | |

| January 1, 2019 | 155,089 |

| December 1, 2019 | 124,072 |

| December 1, 2020 | 124,072 |

| December 1, 2021 | 124,072 |

| December 1, 2022 | 124,072 |

| December 1, 2023 | 124,072 |

| Total | 775,449 |

The Zakat settlement has been provided for through a charge to retained earnings with the corresponding liability included under other liabilities.