Growing Volume Profitably

SAIB grows its business volumes while increasing its profitability by expanding its reach through traditional and non-traditional channels. The Bank also achieves growth through strategic initiatives like expanding its product portfolio and further exploring promising customer segments.

SAIB seeks to grow its business volumes while increasing profitability – this is a core objective of the Bank. The Bank achieves this growth through a variety of means, such as providing exceptional products and services, and providing channels that are increasingly convenient to customers, such as digital channels. Growth can also be achieved through the diversification of the Bank’s product range, targeting select customer segments, and tailoring our service model to serve our customers and to attract new customers. Key to increasing the Bank’s profitability while growing is controlling costs; capital adequacy also needs to be maintained to meet regulatory requirements.

2019 was the first year of operations under the new three-year Strategic Plan. Of the three phases of implementing the plan, the Bank completed the “Transformation” phase early during the year which led to the launching of the Innovation Lab, following an assessment of the Bank’s opportunities and strengths, and identifying the areas for development focus. Thereafter, the Bank moved on to the “Building” phase focussing on developing infrastructure, strengthening foundations, making the necessary changes in operations, executing critical projects and deep-rooting its customer loyalty. It is through the implementation of the “Acceleration” phase that the Bank envisages to reap tangible benefits of the Plan.

This financial review provides an analysis of the financial position, results of operations and cashflows of the Bank during the year 2019. This should ideally be read in conjunction with the Operating Environment and the “investments” made for the implementation of the strategic plan that provided the context within with the performance of the Bank for the year was achieved.

An overview

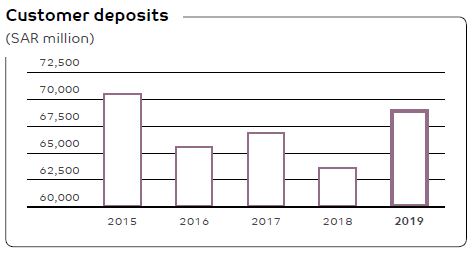

Customer deposits grew by an above industry average growth of 8.43%, enabling the Bank to grow its total assets by 4.94% as at 31 December 2019.

A substantial increase in provisions for credit and other losses more than offset the 3.89% growth in total operating income for the year, leading to 81.89% decrease in operating income. However, at the net income level the decrease was less pronounced at 58.42% as a result of the provision for Zakat and tax liability for 2019 being SAR 90 million only compared to SAR 868 million in 2018 which included a provision for a settlement of Zakat assessments for the years 2005 to 2017 agreed with the GAZT. Reflecting the drop in net income, both the return on average assets and the return on average shareholders’ equity too declined to 0.24% and 2.03% respectively in 2019 compared to 0.61% and 4.73% in 2018.

No dividends have been proposed for the year ended December 31, 2019.

Financial position

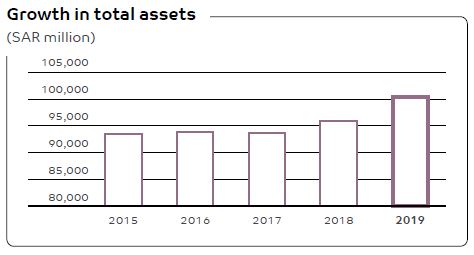

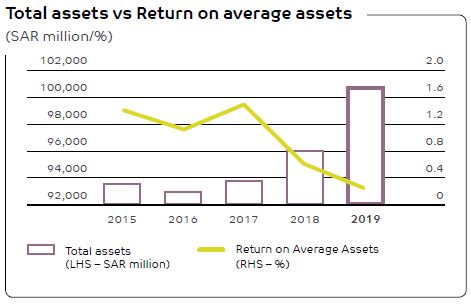

Total assets crossed the milestone of SAR 100 billion to reach SAR 100.8 billion as at December 31, 2019 which was higher by SAR 4.7 billion or 4.89% compared to the December 31, 2018 figure of SAR 96.1 billion.

The five-year trend of SAIB’s share of the total assets of Saudi Banks is given below:

| Year | |||||

| 2019 | 2018 | 2017 | 2016 | 2015 | |

| SAIB’s Market share (%) | 4.12 | 4.24 | 4.22 | 4.26 | 4.31 |

Details relating to movements in total assets are given below.

The Bank’s cash and balance with SAMA amounted to SAR 10.2 billion as at December 31, 2019 compared to SAR 4.9 billion as at December 31, 2018. The increase was primarily due to an increase in overnight placements with SAMA from SAR 977 million on December 31, 2018 to SAR 6.0 billion on December 31, 2019.

The Bank’s investment portfolio totalled SAR 26.2 billion as at December 31, 2019 compared to SAR 24.6 billion as at December 31, 2018, an increase of SAR 1.6 billion or 6.50%. Investments classified by major rating agencies as investment grade represented 86.25% of the total portfolio as at December 31, 2019, compared to 85.15% as at December 31, 2018.

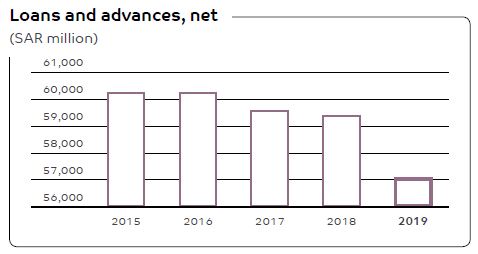

Loans and advances, net as at December 31, 2019 totalled SAR 57.1 billion compared to SAR 59.4 billion as at December 31, 2018, representing a decrease of SAR 2.3 billion or 3.87%. Total performing loans decreased to SAR 57.1 billion from SAR 60.1 billion primarily due to lower consumer loans and overdrafts while non-performing loans increased to SAR 2.4 billion from SAR 1.1 billion following an evaluation of individual exposures considering the ability of the borrowers to repay.

Consequently, non-performing loans as a percentage of total loans and advances increased to 3.99% as at December 31, 2019, compared to 1.76% as at December 31, 2018.

The cumulative allowance for credit losses totalled SAR 2.4 billion as at December 31, 2019 which was 4.04% of total loans and 101.31% of non-performing loans. This compared to SAR 1.8 billion as at December 31, 2018 which was 2.93% of total loans, and 166.74% of non-performing loans. While the expected credit loss coverage of non-performing loans declined in 2019, the credit risk has been adequately mitigated by collateral that the Bank holds against its non-performing exposures.

Loans and advances as at December 31, 2019 include non-interest based banking products including Murabaha agreements, Tawarruq, Istisna’a and Ijarah totalling SAR 39.0 billion, compared to SAR 37.1 billion as at December 31, 2018.

The Bank in the ordinary course of lending activities holds collateral as security to mitigate credit risk on its loans and advances. The collateral primarily includes time, demand, and other cash deposits, financial guarantees, local and international equities, real estate, and other assets. The estimated fair value of collateral held by the Bank as security for total loans and advances is approximately SAR 47.3 billion as at December 31, 2019, compared to SAR 49.4 billion as at December 31, 2018.

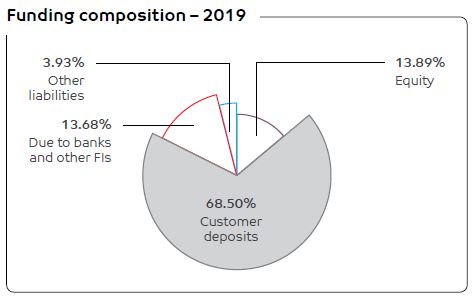

Customer deposits grew to SAR 69.1 billion as at December 31, 2019 compared to SAR 63.7 billion as at December 31, 2018, an increase of SAR 5.4 billion or 8.48%. Demand and other deposits amounted to SAR 27.4 billion accounting for 39.66% of the total deposits as of December 31, 2019 compared to SAR 25.1 billion and 39.45% as of December 31, 2018. Special commission bearing deposits also increased by SAR 3.1 billion or 8.03% to SAR 41.7 billion during the year ended December 31, 2019.

The Bank entered into a five-year medium-term loan facility agreement on June 19, 2016 for an amount of SAR 1.0 billion for general corporate purposes. The facility has been fully utilized and is repayable on June 19, 2021. On September 26, 2017, the Bank entered into another five-year medium-term loan facility agreement for a further SAR 1.0 billion for general corporate purposes. This facility too was fully utilized on October 4, 2017 and is repayable on September 26, 2022.

The term loans bear commission at market based variable rates. The Bank has an option to prepay the term loans subject to the terms and conditions of the related facility agreements. The facility agreements above include covenants which require maintenance of certain financial ratios and other requirements and the Bank has complied with all such covenants as at December 31, 2019. In addition, the Bank has not had any defaults of principal or commission on the term loans.

On June 5, 2014 the Bank concluded the issuance of a SAR 2.0 billion subordinated debt through a private placement of a Shariah compliant Tier II Sukuk in KSA. The Sukuk carried a half yearly profit equal to six-month SIBOR plus 1.45%. The Sukuk had a tenor of ten years with the Bank retaining the right to call the Sukuk at the end of the first five-year period, subject to certain regulatory approvals. The Bank has not had any defaults of principal or commission on the subordinated debt.

Whereas the original maturity date for the Sukuk is June 5, 2024, the Bank redeemed the Sukuk at the optional dissolution date of June 5, 2019 after receiving all required regulatory approvals.

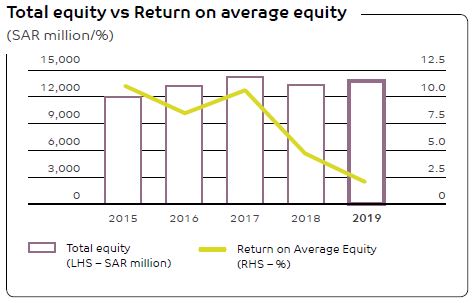

The Bank’s total equity increased to SAR 14.0 billion as at December 31, 2019, compared to SAR 13.4 billion as

at December 31, 2018. Total comprehensive income of SAR 761 million and proceeds from Tier I Sukuk of

SAR 215 million partly offset by the cost of purchasing treasury shares amounting to SAR 254 million and Tier I Sukuk costs of SAR 122 million contributed to this increase.

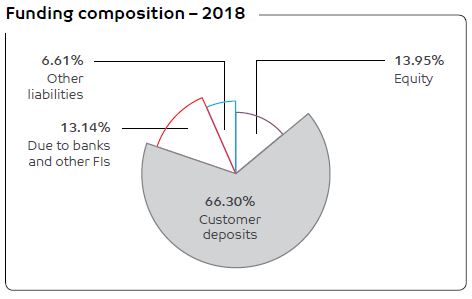

The percentage of total equity to total assets as at December 31, 2019 was 13.89%, compared to 13.95% a year ago. The Bank’s shareholders’ equity leverage ratio was 8.40 times as at December 31, 2019 compared to 8.27 times as at December 31, 2018.

Besides the Treasury shares purchased from JP Morgan International Finance Limited at a cost of SAR 787.5 million in 2018, the Bank entered into a Share Purchase Agreement with Mizuho Bank Ltd (Mizuho) on November 29, 2018, to purchase another 18,749,860 shares of the Bank owned by Mizuho at SAR 13.50 per share amounting to SAR 253.1 million, exclusive of transaction costs and estimated income tax. The Bank received all regulatory approvals for the purchase, and the agreement to purchase the shares was approved at an Extraordinary General Assembly Meeting held on 21 Rajab 1440H, corresponding to March 28, 2019. On May 28, 2019, the Bank completed the purchase. The Treasury shares purchased including transaction costs amounted to SAR 253.5 million.

The share capital of the Bank has not been reduced on account of these transactions with the cost of the shares purchased totalling SAR 1,041.1 million presented as a reduction from shareholders’ equity. The total number of shares outstanding as of December 31, 2019 was approximately 675 million after reflecting the Treasury shares held by the Bank.

The Bank completed the establishment of a Shariah compliant Tier I Sukuk Programme (the Programme) in 2016. The Programme has been approved by the Bank’s regulatory authorities and shareholders. The Bank had issued securities totalling SAR 1,785 million as at December 31, 2018. During 2019, the Bank issued an additional SAR 215 million in securities under the Programme, which now totals SAR 2,000 million as at December 31, 2019.

The Tier I Sukuk securities are perpetual with no fixed redemption dates and represent an undivided ownership interest in the Sukuk assets, constituting an unsecured conditional and subordinated obligation of the Bank classified under equity. However, the Bank has the exclusive right to redeem or call the Tier I Sukuk debt securities in a specific period of time, subject to the terms and conditions stipulated in the Programme.

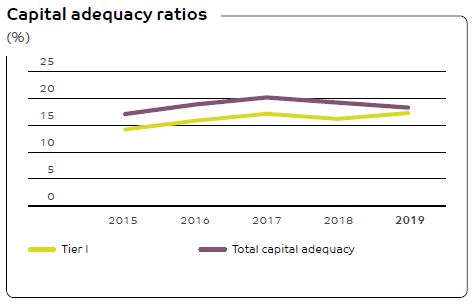

The Bank’s objectives when managing capital are to comply with the capital requirements set by SAMA, to safeguard the Group’s ability to continue as a going concern, and to maintain a strong capital base. Capital adequacy and the use of Regulatory capital are regularly monitored by the Bank’s management and periodically reported to the Board.

As of December 31, 2019, the Bank’s total capital adequacy ratio was comfortably above the minimum regulatory requirement of 10.5%, at 18.26% compared to 19.31% as of December 31, 2018.

Results of operations

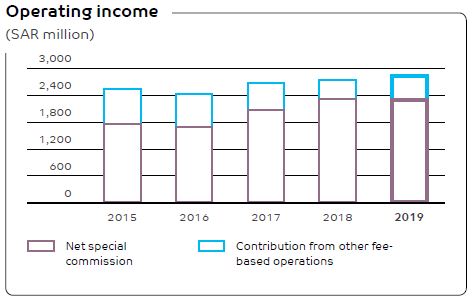

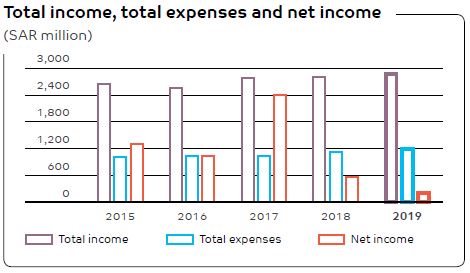

Total operating income for the year grew to SAR 2,818 million compared to SAR 2,713 million in 2018, an increase of SAR 105 million or 3.87%. However, net special commission income from fund-based operations which accounted for 80.84% (84.33% in 2018) of the total operating income recorded a marginal decrease of SAR 10 million or 0.44%. This was due to the growth in special commission income by 7.41% being offset by a higher increase in special commission expense of 20.73%. A negative rate variance of SAR 74 million and a positive volume variance of SAR 64 million contributed to this decrease.

Contribution from fee-based operations to the total operating income amounted to SAR 540 million for the year (SAR 425 million in 2018). Fee from banking services reached SAR 299 million in 2019, compared to SAR 295 million in 2018, an increase of SAR 4 million or 1.36%. The increase was due to higher trade finance and card volumes, and an increase in investment management and brokerage business. Exchange income reached SAR 156 million in 2019, compared to SAR 141 million in 2018, an increase of SAR 15 million or 10.64%. The increase was due to increased volumes in customer FX transactions reflecting the Bank’s coordination between Treasury and its Retail and Corporate clients. There was no dividend income in 2019 compared to SAR 5 million received in 2018. Other investment related gains earned from income recognized through profit and loss and sales of debt securities totalled SAR 54 million in 2019 compared to a loss of SAR 16 million in 2018. All other operating income totalled SAR 31 million in 2019, compared to a small net loss in 2018, contributed primarily by sale of other real estate at favourable prices.

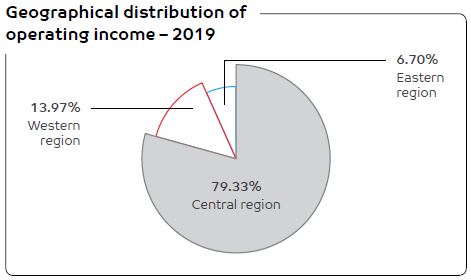

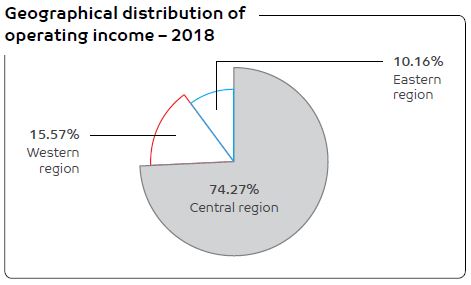

Geographical distribution of operating Income

The Bank’s total operating income is entirely generated from its operations in the Kingdom of Saudi Arabia. A region-wise analysis is given below;

| Central

Region SAR ’000 |

Western

Region SAR ’000 |

Eastern

Region SAR ’000 |

Total SAR ’000 |

|

| 2019 | 2,235,624 | 393,661 | 188,943 | 2,818,228 |

| 2018 | 2,014,781 | 422,442 | 275,507 | 2,712,730 |

Total operating expenses before provisions for credit and other losses increased by SAR 101 million or 8.91% to SAR 1,234 million for the year compared to SAR 1,133 million in 2018. Main contributory factors for the increase were an increase in other general and administrative expenses by SAR 68 million due to the expenses incurred in connection with the Bank’s new Strategic Plan and an increase in depreciation and amortization by SAR 41 million due to depreciation expense relating to Right of Use leased assets recognized as per the provisions of IFRS 16 which stipulates that all leases and the associated contractual rights and obligations should generally be recognized in the consolidated statement of financial position, unless the term is 12 months or less or the lease is for a low-value asset item.

Salaries and employee related expenses for the year remained approximately at the same level as in 2018 despite the head count as of December 31, 2019 being 1,481 only compared to 1,581 a year ago. Rent and premises related expenses recorded a decrease of SAR 8 million compared to 2018 due to the change in accounting for leases as referred to in the earlier paragraph.

Relatively higher increase in operating expenses compared to the increase in operating income resulted in a deterioration in the net efficiency ratio to 41.60% compared to 39.30% in 2018.

Provisions for credit and other losses for the year increased to SAR 1,343 million from SAR 247 million in 2018. This was primarily due to a change in the status of certain loans and advances and the revaluation of associated collateral. The provisions were taken as a precautionary measure to improve the financial position of the Bank in the long term and do not in any way mean that the collection efforts of these loans will be relaxed or discontinued.

The Bank’s share in earnings of associates for the year amounted to SAR 88 million compared to SAR 111 million in 2018, a decrease of SAR 23 million. The decrease was primarily due to the settlement of prior year Zakat liabilities for individual associate companies during 2019.

The provisions for Zakat and Income Tax for the year was SAR 90 million compared to SAR 868 million in 2018 primarily due to the recognition of a provision of SAR 751 million for Zakat liabilities for the years 2005 to 2017, in 2018 consequent to a settlement agreed with GAZT. A summary of the provisions for Zakat and Income Tax in 2019 compared to 2018 is given below:

| 2019 SAR ’000 |

2018 SAR ’000 |

|

| Provision for Zakat: | ||

| For the current period | 76,809 | 89,305 |

| For years 2005-2017 | – | 750,506 |

| For subsidiaries for years 2011-2017 | 3,300 | – |

| Provision for income tax: | ||

| For the current period | 1,800 | 28,060 |

| For prior periods | 8,131 | – |

| Provision for Zakat and Income Tax | 90,040 | 867,871 |

The provisions for Zakat in 2019 also reflect the effects of changes in the method of calculating the Bank’s Zakat liability which were published by the General Authority of Zakat and Tax (GAZT) in 2019.

The Bank reported net income of SAR 239.5 million for the year ended December 31, 2019, a decrease of SAR 336.4 million, or 58.41%, compared to SAR 575.9 million reported for 2018. The singular most factor for the drop in net income was the substantial increase in provisions for credit and other losses for the year.

Reflecting the drop in net income coupled with the increase in average assets and average shareholders’ equity, both the return on average assets and the return on average shareholders’ equity too declined to 0.24% and 2.03% respectively in 2019 compared to 0.61% and 4.73% in 2018.

In accordance with Saudi Arabian Banking Control Law and the Articles of Association of the Bank, SAR 60 million representing 25% of the annual net income was transferred to the statutory reserve, which is not currently available for distribution.

In 2018, the Board of Directors proposed a cash dividend of SAR 450 million equal to SAR 0.60 per share, net of Zakat withheld from the Saudi shareholders. The proposed cash dividend was approved by the Bank’s shareholders at an Extraordinary General Assembly Meeting held on April 24, 2018 (corresponding to 8 Shaban 1439H). The net dividends were paid to the Bank’s shareholders thereafter. No dividends have been proposed for the year ended December 31, 2019.

Income before provisions for Zakat and Income Tax of the Bank’s reportable operating segments for the years ended December 31, 2019 and 2018 is given below:

| 2019 SAR ’000 |

2018 SAR ’000 |

|

| Retail Banking | (622,959) | 247,461 |

| Corporate Banking | 601,148 | 833,902 |

| Treasury and Investments | 559,557 | 531,841 |

| Asset Management and Brokerage | 33,832 | 10,607 |

| Others* | (242,077) | (180,043) |

| Income before provisions for Zakat and income tax | 329,501 | 1,443,768 |

*Others include the net results related to Information Technology, Operations, Risk, and other support units.

Cash flows

Cash and cash equivalents grew by SAR 5,110 million during the year from SAR 4,503 million as at December 31, 2018 to SAR 9,613 million as at December 31, 2019. The principal reasons for this increase are given below;

| Cash flows from: | 2019 SAR million |

2018 SAR million |

Principal reasons |

| Operating activities | 8,239 | 2,616 | Growth in deposits by SAR 5,385 million as against a decrease in deposits by SAR 3,251 million in 2018. |

| Investing activities | (968) | (3,277) | Cash outflows on investments being SAR 2,858 million only as against SAR 5,072 million in 2018. |

| Financing activities | (2,161) | (280) | Redemption of subordinated debt of SAR 2,000 million |

| Net increase in cash and cash equivalents | 5,110 | (941) |

In 2019, the Bank achieved a number of key milestones. The Bank continued developing products and services for its different segments in pursuit of fulfilling its customers’ needs and expectations. The Bank is managed on a line-of-business basis. Transactions between business segments are conducted on normal commercial terms and conditions through the use of funds transfer pricing and cost allocation methodologies. A detailed analysis of performance of the operating segments in 2019 and 2018 is presented in Note 28 to the Consolidated Financial Statements.

The Bank has three significant business segments, each of which is described below.

Retail Banking offers conventional and Shariah compliant retail products and services for individuals, through the Head Office and a network of 52 branches throughout Saudi Arabia, of which 10 have ladies sections, as at December 31, 2019. In addition, the Bank currently operates a network of 393 ATMs and Interactive Teller Machines, Interactive Voice Recognition (IVR), more than 9,300 POS terminals throughout Saudi Arabia and online banking (Website and Mobile Applications). Services offered by Retail Banking include current accounts, savings, and time deposit accounts. The Bank also offers Shariah compliant products through its Shariah compliant branches.

Corporate Banking serves the financial needs of a range of business establishments from micro, small, and medium enterprises (MSMEs) to large corporate entities. Corporate Banking operates from three regional headquarters based in Riyadh, Jeddah, and Al-Khobar as well as through Syndications, Project, and Structured Finance Departments to provide tailor-made financial solutions and highly customized structures. Corporate digital banking services currently have multiple distribution channels including corporate online banking, eTrade, ePayroll, Cash Management, and B2B services.

Corporate Banking offers both conventional and Shariah compliant products and services and include facilities related to working capital financing, contract financing, project financing, syndicated financing, real estate financing, capital financing, trade finance, cash management, and treasury services for corporates. It continually strives to increase the range and quality of the Bank’s product and service offerings to meet customers evolving needs and expectations.

Treasury and Investment is responsible for the Bank’s Asset-Liability Management including interest rate risk, market risk, and funding and liquidity management. It also manages foreign exchange trading, structured products, as well as managing the Bank’s Investment portfolio and derivative products. Treasury and Investment also manages the Bank’s Business Partner Companies, Financial Institutions, Public Institutions, and the Asset Liability Management unit.

Credit ratings

Credit ratings are an integral component for participation in the international financial markets. As the global economy becomes more integrated, credit ratings are necessary not only to ensure funding and obtain access to capital markets, but also to demonstrate a commitment to meeting a high level of internationally recognized credit and risk management standards.

During the year, rating reviews were conducted by Standard & Poor’s Ratings Services (S&P), Moody’s and Fitch Ratings. A summary of the Bank’s current ratings is given below:

| Long-term | Short-term | Outlook | |

| Moody’s | A3 | P-2 | Stable |

| S&P | BBB | A-2 | Stable |

| Fitch | BBB+ | F2 | Stable |

The Bank’s stable ratings are the outcome of its financial performance, asset quality and capitalization levels, supported by a robust strategy and adequate funding and liquidity profile. Our ratings also take into consideration the fact that the Bank operates in one of the strongest banking sectors and best regulated markets in the Middle East. The ratings also reflect Saudi Arabia’s sovereign credit ratings from Moody’s, Fitch, and S&P, in addition to the country’s economic fundamentals, adherence to BIS norms, and G20 alignment.