Operating Environment

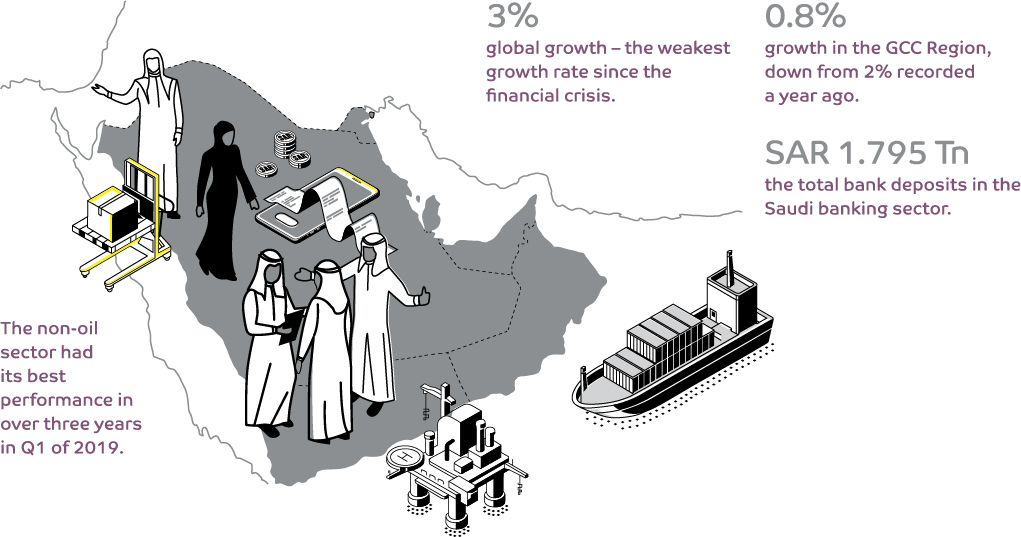

The global economy slowed down to 3%, the weakest growth rate since the global financial crisis, a result of trade barriers and increasing uncertainty. While advanced economies and smaller Asian advanced economies have weakened, emerging market and developing economies (EMDEs) have been hit harder by the global slowdown. The US economy settled into a slower pace of expansion, as did the UK as investment declined due to uncertainty over Brexit, while weak export activity continued to hamper the growth of the Euro area economy. A decline in industrial output was observed across the globe, as both firms and households became more reserved in purchasing machinery, equipment, and durable goods, thus contributing to the slowdown in global trade. However, services activity held steady and helped to maintain employment creation, which in turn bolstered consumer confidence and household spending on services. Energy prices declined during the year as the US ramped up production to a record high and demand slowed. Central banks reacted to the slowdown by cutting interest rates, thus lessening its impact. However, the slow growth is expected to continue well into 2020 and 2021.

The countries of the Gulf Cooperation Council (GCC) were not immune to the impacts of the global economy and had to deal with geopolitical issues that raised the risk perceptions of the region; the GCC economy is projected to have slowed down significantly to 0.8% from 2% in 2018. The continued slowdown experienced by China and global trade war hindered efforts to boost non-oil exports, although non-oil sectors experienced a healthy growth as a result of extensive public investment programmes around transportation, energy, and logistics infrastructure. Moreover, GCC governments have been working diligently to diversify their economies and implement progressive reforms to be more conducive to foreign investment and trade. Value added tax (VAT) and excises have also helped to diversify sources of fiscal revenue. The outcome is that three of the top 10 global improvers on the World Bank’s Doing Business Indicators reside in the GCC – Saudi Arabia, Bahrain, and Kuwait.

The economy of the Kingdom of Saudi Arabia is projected to have slowed down to an estimated 0.4% in 2019. The economy slowed down sharply in the first half of 2019 as a result of significant cuts to oil production as part of an OPEC+ agreement and a reaction to increased US shale production. The country’s oil production was once again disrupted by the attacks in September. The country is still largely dependent on its oil exports, which significantly outweigh its non-oil exports that represent just 17% of total exports. However, the non-oil sector had its best performance in over three years in Q1 and helped to pick up the slack from the contraction of the oil sector in Q2. The services sector, which represents approximately 40% of the country’s economy, accounted for most of the non-oil growth. Fiscal deficits were prevalent across most of the GCC and Saudi Arabia was no different, with the government loosening its fiscal policy stance and increasing spending; this combined with the reduced oil revenue growth has led to a projected fiscal deficit of 4.7% of the GDP for 2019. Inflation in 2019 is projected to be 1% and is expected to hit 2% in 2020 as economic growth continues to perform below potential. Moreover, public finances are expected to remain in deficit for the near future.

The outlook for 2020 is looking to trend upwards, with a projected economic growth of 2.2% for the GCC, assuming that oil prices recover and spending on mega-projects and growth in non-hydrocarbon sectors continues. Monetary, fiscal, and structural policies being geared to expand the private non-oil sector GDP in the medium-term is expected to lend a boost to the economy of Saudi Arabia in 2020 to an estimated 2.2%. Although the Saudi Arabian Government is working to diversify the economy away from oil, it is also committed to leveraging its oil resources by focusing investment towards downstream activities such as oil refining and petrochemical production. Many projects are reliant on the Public Investment Fund (PIF) for financing, which itself should see a significant liquidity boost as a result of the initial public offering of Saudi Aramco. The non-oil private sector is also expected to receive a boost from the G20 summit in 2020, which is being hosted for the first time in the Middle East by Saudi Arabia. Ultimately, the growth of the global economy will be subject to the impact of trade tensions, geopolitical risks, as well as the outbreak of COVID-19, whose impacts are yet to be ascertained. These external risks could also affect Saudi Arabia’s economy, along with rising geopolitical tensions and erratic oil price fluctuations.

Saudi banking sector

Total bank deposits in the Saudi banking sector increased by 7.3% in 2019, reaching SAR 1.795 trillion up from SAR 1.674 trillion in 2018. Demand deposits constituted 61.2% of the total and grew 5.6% year on year to SAR 1.099 trillion Savings and term deposits also saw a 13.2% year on year increase to SAR 501.67 billion. The banking sector’s aggregate income grew 5% to SAR 50.5 billion and aggregate assets increased by 10% to SAR 2.631 trillion. Money supply in the Saudi banking sector was boosted by the proceeds of Saudi Aramco’s initial public offering, and Saudi banks increased money lending during the year as a result of the government-backed mortgages programme. Growth was seen in Bank credit during the year, a 7.6% year on year increase to SAR 1.552 trillion, up from SAR 1.443 trillion in 2018. Long-term credit increased by 26.7% to SAR 634.64 billion by the end of 2019, while medium-term credit increased by 2.9% and short-term credit increased by 4.4%. The credit-deposit ratio for the year was recorded at 86.44%. However, credit demand is challenged by the operating environment and GDP growth – the economy is still highly dependent on oil, despite ongoing diversification efforts.