How can we help you navigate better through our Integrated Report?

Select the topic that most interests you from the choices and we will suggest suitable sections from our Report that you could read.

About the BankLearn about the Bank’s strategyLearn about the Bank’s governance policies, practices and standardsThe Bank’s financial performanceStatements from senior decision-makers of the BankRelationships with customers, business partners and investorsThe Bank’s environmental and societal commitment

Growth prospects in the global economy have been somewhat dampened in 2018. However, growth in GCC countries is expected to accelerate, driven by higher oil prices and eased fiscal consolidation.

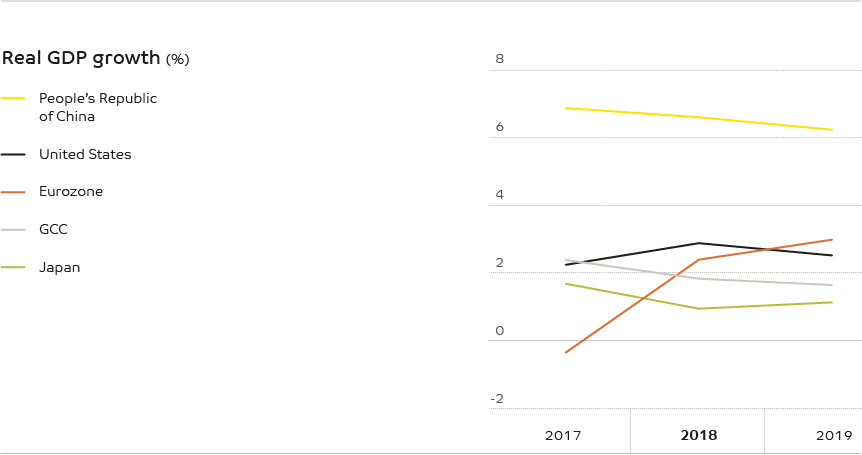

Growth in the global economy in 2018 is estimated to be 3.7%, while the growth forecasts for 2019 and 2020 are 3.5% and 3.6% respectively. The 2019 and 2020 figures are a slight downward revision of previous forecasts. The U.S. imposed trade barriers on imports from China and some other countries during the year. The trading partners are expected to retaliate if they have not already done so. These developments and uncertainty over policy have resulted in dampening of growth. Uncertainties regarding future growth tend to more on the negative side, due to fears of escalating trade tensions.

A “no deal Brexit” continues to be another threat.

The U.S. economy received a boost from income and business tax cuts. Growth was expected to peak at 2.9% in 2018 but is expected to reduce to 2.5% in 2019. Capacity constraints are expected to constrain growth in the immediate future. This is likely to cause an increased demand for imports which, together with tariff barriers, will add to domestic price pressures. There is also a shortage of skilled workers and professionals in certain categories. Higher input costs are bound to push up consumer prices before long.

The Eurozone is expected to record a modest growth of 1.8%. Growth has been hampered by soft private consumption and reduced production due to revised auto emission standards in Germany; due to political and industrial unrest in France; and due to weak demand and higher borrowing costs in Italy. In Japan the economy has been affected by higher oil prices and a shortage of labour, but was expected to record a moderate 0.9% 2018 and 1.1% 2019.

The large East Asian economies are expected to record only moderate growth, by past standards, due to the impact of external factors. China’s growth was constrained by slower expansion in industrial production and fixed assets, and is estimated to reduce to 6.6% in 2018. A further reduction to 6.2% in 2019 is anticipated. While export performance has remained robust, indications are that growth will be dampened by rising trade barriers and weakened credit growth. The economic outlook in India is positive with annual growth of 7.3% in 2018 and 7.4% in 2019 being forecast. Growth has been driven by private consumption, more conducive fiscal policies and previous reforms coming to fruition. Growth in Russia is estimated to increase to 1.7% from 1.5% mainly due to higher oil prices and increased domestic demand.

An important non-economic factor has been that technology has been driving changes in job skills and creating needs for regular re-training. Another important consideration for the banking industry is the growing concern about data security and cyberthreats.

GCC

Growth in GCC countries is expected to accelerate in 2019 driven by higher oil prices and eased fiscal consolidation which will uplift domestic demand. An overall growth of 2.4% in 2018 and 3.0% in 2019 is expected, compared with a 0.4% contraction in 2017. However tighter monetary constraints are expected to dampen some of the positive impacts of expansionary fiscal policy. Higher oil prices than those of the previous year, are expected to enhance the balance of payments, with the combined current account surplus being expected to rise to USD 169 billion in 2018.

For the region as a whole, non-hydrocarbon growth has been gradually increasing and is expected to record 3.2% by 2020. Public spending was expected to increase by 15% in 2018, but this should be compensated by higher oil prices and increase in non-hydrocarbon sector revenues leading to a narrowing of the consolidated fiscal deficit. All countries in the region face challenges in diversifying economies and government finances, and are also affected by regional political tensions. While there have been ambitious plans for economic integration among the GCC countries actual progress on the ground has been relatively slow.

Growth in GCC countries is expected to accelerate in 2019 driven by higher oil prices and eased fiscal consolidation which will uplift domestic demand. An overall growth of 2.4% in 2018 and 3.0% in 2019

is expected.

In 2017 the Saudi government mounted major reforms to reduce the economy’s dependence on oil and increase the contribution of the private sector. The latter is one of the main goals of Vision 2030. Fiscal consolidation measures including VAT were introduced.

The GDP was projected to grow by around 2% in 2018 and 2019 (2017: negative 0.7%), as a result of higher oil prices, relaxing of production constraints and increased consumer spending. The current account surplus was expected to be around 10% of GDP in 2018 mainly as a result of oil export revenue. The fiscal position is also showing a positive trend due to reduced fuel subsidies, increased electricity tariffs and reduced oil prices. The budget deficit is expected to reduce to 4.1% and 1.9% of GDP in 2018 and 2019 respectively. Non-oil GDP is also showing a substantial growth, and year on year growth in non-oil exports registered 26% in April 2018. VAT and other taxes have also resulted in a growth in non-oil revenues.

Consumer price inflation was expected to be around 3% in 2018, consequent to the introduction of VAT and price increases but is expected to stabilize at around 2% in 2019. The adoption of Vision 2030 has brought about heartening developments including improving the business environment, developing the SME sector, deepening capital markets, increasing participation of women in the economy and developing industries with high growth potential. The opening of the stock market to foreign investors and creation of a parallel market for the SME sector have been initiatives which augur well for the future.

While the outlook is generally positive, there are some uncertainties that remain. While banks remain well capitalised and liquid there are some doubts about the degree of confidence of investors. There is also an issue of inadequate labour to support certain sectors. While there has been a departure of expatriate labour, employment creation for nationals has not been as rapid as expected and employment in the private sector has declined for the first time since 2005. Matching the available jobs with the type of jobs Saudis are seeking remains a problem. The government continues to employ about 70% of employed Saudis. There are also doubts as to how far the economy will be able to diversify away from oil in the short or medium term.

Oman’s economy, which contracted by 0.9% in 2017, showed a marked recovery in 2018. Oman was expected to achieve an increase in GDP growth, to 2.3% in 2018 and 2.5% in 2019. Growth will be driven by increased prices of oil, increased production of gas and lifting of OPEC restrictions. Fiscal and current account deficits have continued to be in the double digits due to lags in adjusting to lower oil prices. High unemployment remains a major challenge with general unemployment of 17% and youth unemployment of 49%. Diversification efforts are expected to bring results in the tourism, logistics, manufacturing and renewable energy sectors in the long term.

Kuwait too suffered a difficult year in 2017, but growth of 1.5% is estimated in 2018 and a higher growth in 2019 as curbs on oil production are relaxed. Rising public sector employment has boosted household spending. The implementation of VAT, scheduled for 2018 has been postponed to 2021. However, the economy continues to suffer from excessive dependence on hydrocarbon products; while there has been growth in the non-oil sector, about 60% of GDP, over 90% of exports and over 90% of fiscal receipts is drawn from such products.

Bahrain was expected to record a GDP growth of 2.6% in 2019, driven by higher oil production and major projects especially expansion of industrial capacity. Increase in oil prices should lead to a reduction in fiscal deficit and current account deficit. In the longer term there is optimism due to the discovery of new hydrocarbon reserves. The implementation of VAT is scheduled to begin in 2019, dampening growth somewhat and increasing consumer price inflation temporarily.

The UAE economy was expected to pick up in 2018 with GDP growth of 2%, rising to 3.2% by 2020 after a depressed performance in 2017. However, inflation is expected to rise to about 4.2%, mainly due to the introduction of VAT, but this should moderate later. Oil production increased in 2018, due to a revised OPEC deal and there will be the benefits of higher prices. Growth will be driven by oil prices, expansionary fiscal policy, pickup in trade and tourism and in investment in anticipation of Expo 2020 in Dubai.

While in 2017 the Saudi Arabian economy contracted slightly, the GDP is projected to grow by around 2% in 2018 and 2019 as a result of higher oil prices.

Vision 2030

Vision 2030 was the blueprint for Saudi Arabia’s future that was unveiled in 2016. The plan is built on three pillars; Saudi Arabia’s historic position as the heart of the Arab and Islamic world; our determination to become a global investment powerhouse; and leveraging our geographic location to become a hub connecting three continents. There are also three themes woven round the pillars.

A vibrant society – one that would progress and modernise while keeping our religious and cultural heritage

A thriving economy- this would be built based on education and skills development

An ambitious nation – this would be achieved through good governance, transparency and responsibility

Vision 2030 envisages developing and diversifying the economy; reducing the dependence on oil and increasing our global competitiveness are key objectives. The part the private sector plays is to be expanded and it is expected that more foreign investment will flow in. It is also proposed to expand the role the SME sector plays in the economy, thereby developing the entrepreneurial skills of Saudis. We will leverage the untapped skills of Saudi women bringing more of them into the workforce. Educational reforms will be introduced and we will develop some of our universities into world class ones; our major cities will rank among the best in the world.

Saudi banking sector*

The Saudi Banking Sector consists of 12 listed banks and several non-listed banks. The four largest banks account for 56.6% of total assets. Four of the banks are Shariah compliant and account for 27.6% of total assets. In 2018 the total assets of banks increased by 2.1% to SAR 2,331 billion. Saudi banking deposits and money supply grew at a 10-year CAGR of 7.6 % each.

Demand deposits increased by 4.5% in 2018 from SAR 977.8 billion in 2017 to SAR 1,022.3 billion in 2018. Of total deposits, demand deposits accounted for 62.5% while time and savings deposits accounted for 26.0%. Businesses and individuals held 89% of demand deposits while government entities held the remaining 11%. For time and savings deposits the corresponding figures were 58.5% and 41.5% respectively.

The total loans of Saudi Banks registered an increase of

1.5% in 2018 and reached SAR 1,430 billion. The 10-year

CAGR was 6.8%. About 49.3% of the loans have a maturity

period of less than one year (2017: 51.4% ). Loans with a

maturity of 1-3 years fell by 10.3% year on year and their

share of the total fell from 18.3% from the previous year to

16.1%. A high concentration of short-term loans in a rising

interest rate environment is advantageous to banks as loans

can be re-priced.

In terms of loans by sector the commerce sector, leads with 19.8% of total loans followed by the manufacturing sector (12.2%) and the construction sector (7.2%). Retail loans increased by 3.5% over 2017 to SAR 329.5 billion. The largest segment by loan purpose is home renovation loans accounting for 8.1% of retail loans. Real estate loans grew at a CAGR of 18.6% over the year and reached SAR 217.3 billion.

The Sector’s non-performing loan ratio stood at 1.63% in 2018 as against 1.33% in 2017. The loans to deposits ratio decreased to 86.9% from 87.1% year on year. The banking sector’s operating income increased by 6.2% from SAR 21.8 billion 2017 to SAR 23.1 billion. The retail sector accounted for 47.3% of total operating income (2017: 45.1%). The corporate sectors share was 28.5% (2017: 30.7%). Treasury income increased by 3.3% while investment income increased by 14.6%.